The Polymarket Question

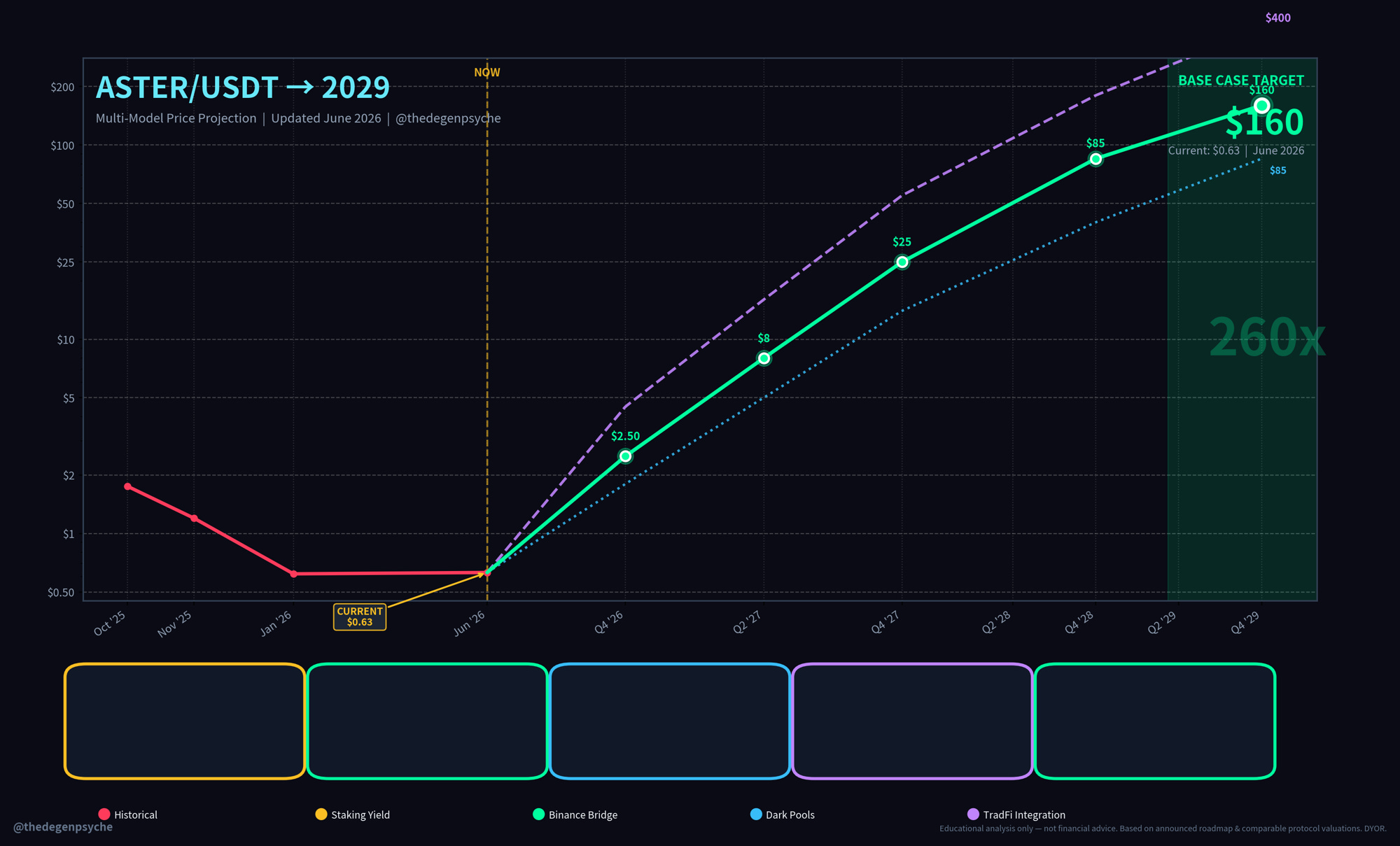

ASTER AD ASTRA

Polymarket spent five years building the most permissive prediction-market platform in crypto, and the last six months watching that permissiveness get dismantled jurisdiction by jurisdiction. The story is worth holding in mind right now because the same regulatory wave that swept Polymarket is going to wash through every DEX that has built its user base on the open-global model, and the projects that survive that wave will be the ones positioned ahead of it, with structural protection that the loud venues currently riding the cycle do not have. AKA, the ones that are backed by the supreme leader, our beloved big cousin, CZ.

The Polymarket Year

Polymarket paid the CFTC $1.4 million in 2022 for operating an unregistered derivatives exchange, then spent the next three years building a US-compliant arm by acquiring the CFTC-licensed QCEX exchange and relaunching for US users in late 2025 under an invite-only waitlist. The international side of the business kept running on the older open model until 2026 happened. Spain ordered ISPs to block Polymarket and Kalshi. Indonesia, France, Brazil, India, Australia, and the UK each issued their own restrictions or bans. Nevada filed a civil complaint and Tennessee issued shutdown orders in the same week of January. Massachusetts ruled in court that prediction market contracts function as illegal sports wagering under state law. The list now sits at over thirty countries with full or partial restrictions, and the platform has responded by implementing aggressive VPN blocks, IP-based geofencing, and tighter identity verification across its international footprint.

The shift from “open and global” to “compliant and restricted” happened in months rather than years. Users who had been trading without friction for years suddenly found themselves locked out or pushed through KYC. The Polymarket token, separate from the platform itself, has spent 2026 absorbing the price impact of every new jurisdiction that closed its doors. The pattern is the regulatory equivalent of a slow-motion liquidation, and it is not finished.

Hyperliquid Is The Next Domino The Market Has Not Priced

Hyperliquid is the venue most likely to take the next major regulatory hit, and the market has not yet absorbed how exposed it is. The platform restricted US users from day one through its terms of service, which is often cited as a defensive posture, but the depth of the restriction is shallower than retail observers assume. Hyperliquid does not run KYC, which means the geographic enforcement relies on IP blocks and user attestations that any motivated trader can route around with a VPN. The platform’s own traffic data shows that 22.59 percent of its user base sits in the United States, which is the largest single country source by a wide margin. That is the same structural problem that produced the CFTC settlement for Polymarket in 2022, dressed in a different jurisdiction-of-origin claim.

In May 2026, CME Group and ICE sent formal letters to the CFTC and Congress requesting an investigation into Hyperliquid over manipulation risk and potential sanctions evasion. Bloomberg covered the letters as a serious regulatory escalation. Hyperliquid responded by establishing a $29 million Washington policy operation to lobby for a US perps framework, which is the kind of defensive spending that a platform commits to when its founder rather not go to jail.

HYPE has been moving (or rather “dumping”) in patterns that confirm the underlying instability. HYPE traded at an all-time high of $64.63 on May 26, 2026, after a 70 percent rally over the preceding ten days. Tokens that rally that fast tend to give back the gain on the same timeline. The token has scheduled supply unlocks ahead, with a $375 million unlock that hit in April 2026 and further unlocks structured into the emission schedule. The ETF flows that launched in May are real, and two ETFs of a single asset trading with daily volume swings of forty to fifty percent against their first-week baselines tells institutional allocators that they are looking at early-stage volatility rather than settled demand, and the allocator's response to early-stage volatility is to wait

Add the James Wynn liquidation cascade from May 2025, where he/him lost roughly $100 million on a publicly visible billion-dollar Bitcoin long, and the visible-order-book vulnerability that Wynn’s situation surfaced becomes the platform’s most cited structural weakness. CZ himself called for dark-pool style perpetual trading on DEXes after the Wynn incident, and the lack of order privacy on Hyperliquid was the specific problem he was pointing at. Eighteen months later, Hyperliquid still does not have a credible hidden-order solution in production.

The picture this assembles is of a platform that is dominant today, exposed structurally on multiple fronts, and operating in the eye of a regulatory storm that has not yet broken but is visible on the horizon. The market is pricing Hyperliquid as the consensus winner of the perp DEX category, and the structural facts complicate that pricing by reframing the asset as the consensus winner of a single competitive cycle rather than of the broader contest.

Why Aster Is The Cleaner Long-Term Position

Aster was built into the post-Polymarket regulatory environment from the start, and the design choices show the lesson having been learned. The terms of service include geographic restrictions and a no-circumvention clause from day one, which puts the project on the same formal footing as Hyperliquid. The actual protection runs deeper than the formal language though, and it sits in the structural position the project occupies inside the Binance network.

Aster came out of the Binance orbit by deliberate design. YZi Labs, which is the rebranded Binance Labs, backed the project from inception. The CEO, Leonard, came from a Binance background, and the broader team includes ex-Binance members. CZ personally bought $2 million of ASTER tokens in November 2025 and publicly endorsed the launch, comparing his own purchase to his early acquisition of BNB during the first Binance token generation event eight years earlier. Binance Wallet integrated Aster’s perpetual futures trading directly into its interface in January 2026, which means the largest distributed self-custody wallet in the Binance network now defaults its users into Aster perps without requiring them to leave the Binance product surface.

None of these connections are subtle, and none of them are accidental. What they produce is something Polymarket never had and Hyperliquid does not have, which is a project sitting inside the political and regulatory shadow of the largest exchange in crypto. Binance has spent the past three years building a US regulatory posture through its DOJ settlement and its ongoing compliance work, and the projects that share its network benefit from that posture indirectly. When a regulator considers action against an Aster-style venue inside the Binance network, the action is not against an isolated startup with no legal capacity. It is against a venue connected to an actor with significant lobbying resources, established legal counsel, and the kind of institutional weight that makes regulators think twice about which battles to pick.

The product side reinforces the structural advantage. Aster launched Hidden Orders eighteen days after CZ’s call for dark-pool DEX trading, becoming the first perpetual DEX to implement a credible cryptographic dark pool. That is the exact product that institutional traders need to move size without getting hunted on public order books, and it is the product Hyperliquid still does not have. Aster’s hidden-order architecture uses a commit-and-relay mechanism that conceals order intent until execution while still tapping the main liquidity book, which solves the institutional-flow problem without fragmenting liquidity into a separate venue.

The result is a project that is destined for the kind of capital that does not move into Hyperliquid because of the visibility problem, and that sits inside the political shadow of the actor most likely to win the regulatory contest of the next two years. But you need to be smart to see this.

The Holding Picture

The honest holding picture across the three platforms looks like this. Polymarket is the cautionary tale of a project that built on the wrong assumptions about regulatory tolerance and is now paying the cost. Hyperliquid is the loud consensus winner of the current cycle, with serious structural exposure to the regulatory and competitive pressure that the next two cycles will produce. Aster is the project positioned for the world that comes after the wave breaks, with the political backing, the product design, and the distribution surface to absorb the flow that the other two cannot hold.

The macro frame from the previous article in this publication still applies. CZ does not lose, and the projects he has staked his return to active operation on are the ones he is prepared to fight for. Polymarket is an example of what transpires when there is nobody to fight for a project. Hyperliquid is the example of what happens when a project tries to fight alone. Aster is the example of what happens when the fight is structured before the regulatory pressure arrives, with the actor who decides these contests already standing inside the venue.

When the regulatory wave finishes washing through the DEX category, the venue that absorbs the flow is the venue that was positioned for it in advance.

That venue is Aster.